Back to Main Page

Analysis of the "Flash Crash"

Date of Event: 20100506

Part 4, Quote Stuffing

Analysis of the "Flash Crash"

Date of Event: 20100506

Part 4, Quote Stuffing

| While analyzing HFT (High Frequency Trading) quote counts, we were

shocked to find cases where one exchange was sending an extremely high number

of quotes for one stock in a single second: as high as 5,000 quotes in 1

second! During May 6, there were hundreds of times that a single stock had over

1,000 quotes from one exchange in a single second. Even more disturbing, there

doesn't seem to be any economic justification for this. In many of the cases,

the bid/offer is well outside the National Best Bid/Offer (NBBO). We

decided to analyze a handful of these cases in detail and graphed the

sequential bid/offers to better understand them. What we discovered was a

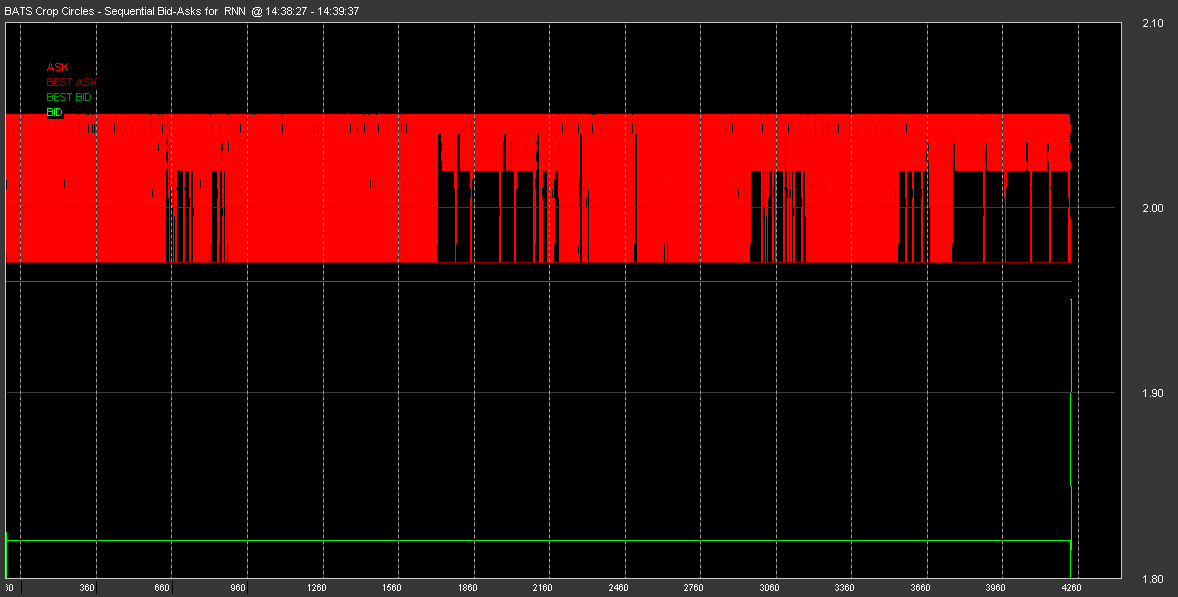

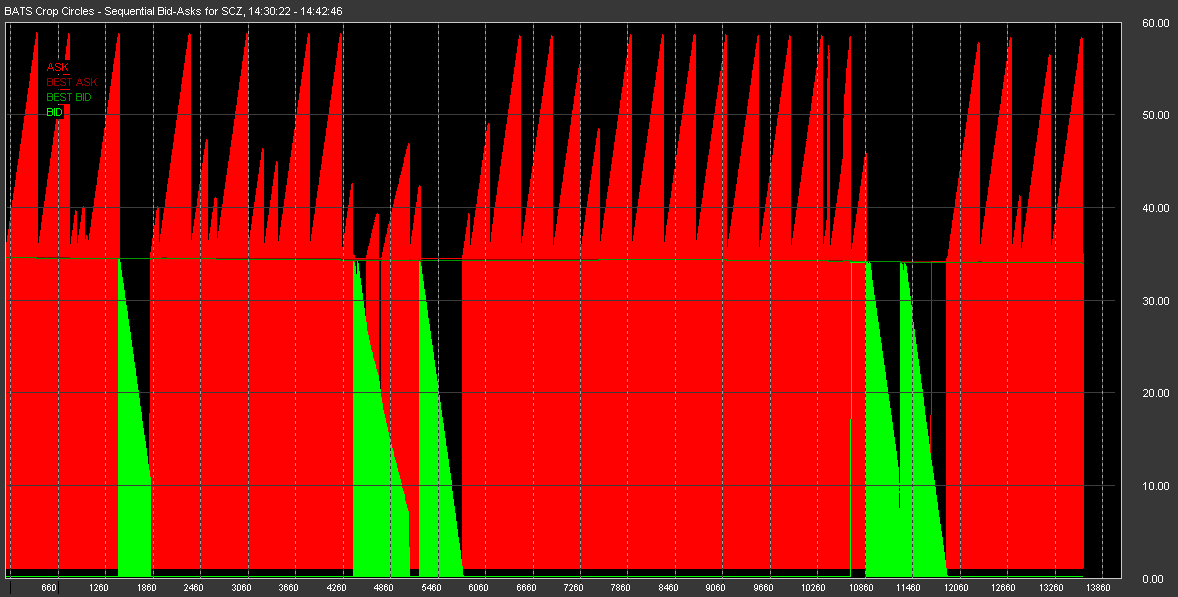

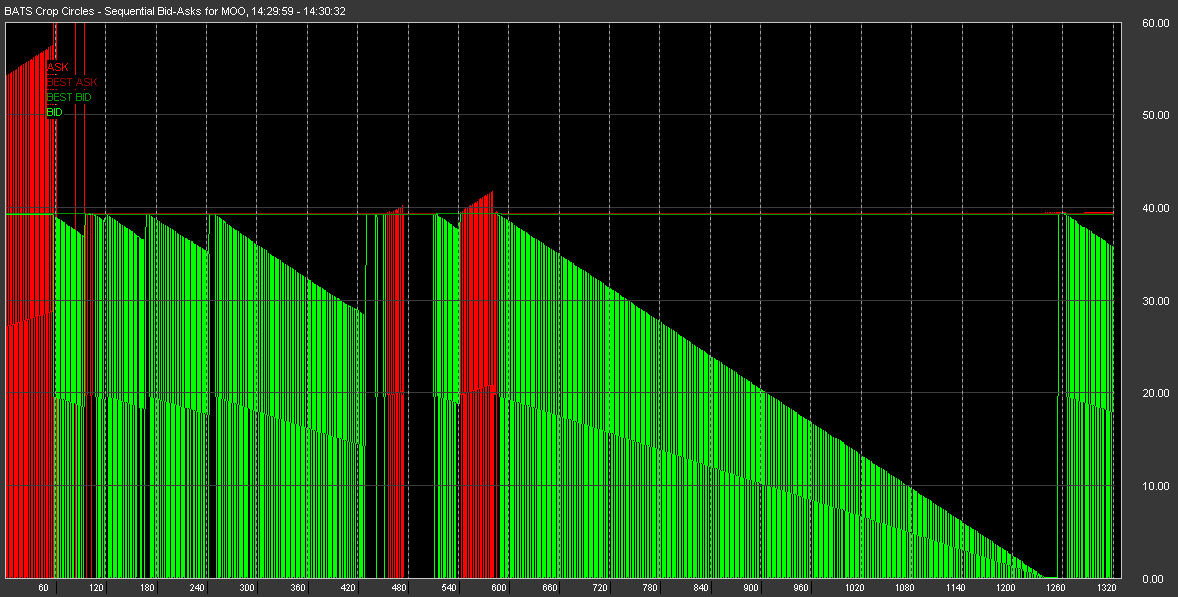

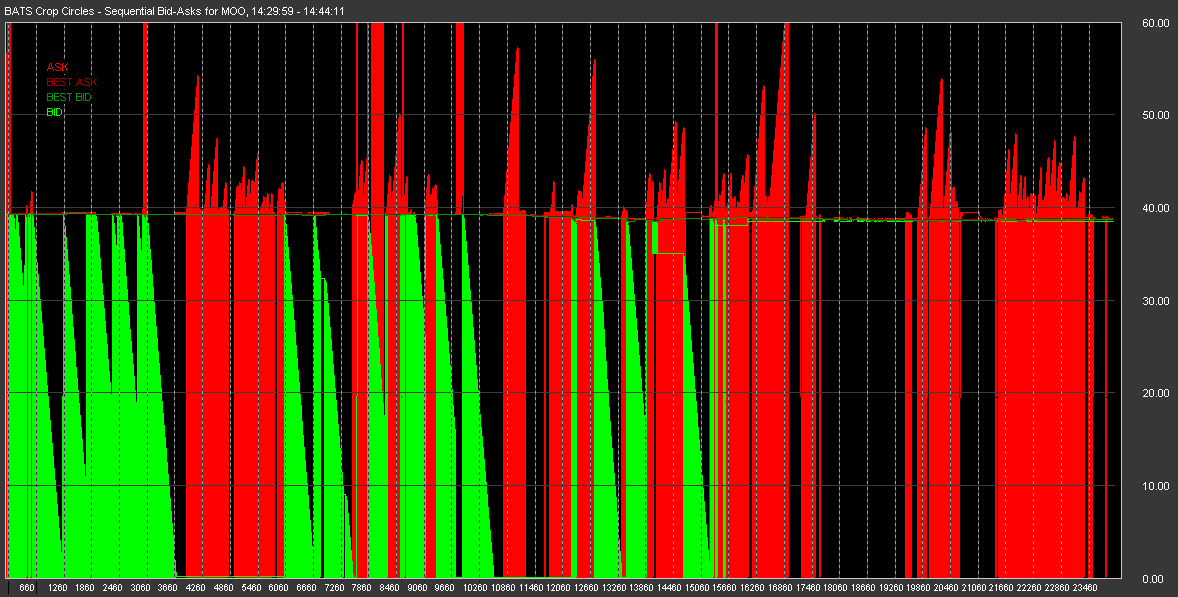

manipulative device with destabilizing effect. The fingerprints of these quote stuffing sequences are evident when looking at specific and unusual bursts of quote data.. The burst will often occur within a 1/2 second or less time frame and can represent literally thousands of quotes within the burst. As time frames are so short, it is easy to see how these extremely unusual bursts of data may go unnoticed and even when this unusual data is found, it must be looked at graphically to understand exactly how unusual it is. In the following data sets, every quote listed or charted was received as a "normal", valid quote (IE quote Condition 0, a valid price and size on both sides of the quote). The one exception is the obvious intermittent "stub" quotes reported by BATS, in which the price will flip from 0.001 to a price near the actual BBO (near being a relative term for BATS) and back again. While the stub quotes actually ARE denoted as a normal quote in the stream, they are in fact the method used by BATS to denote a stub quote. It is worth emphasizing the following charts represent a mere handful of stocks where this quote stuffing occurred on 5/6/2010. These were randomly chosen from a large list of possibilities and provide a good representation of the phenomena. Quote stuffing is also not a rare occurrence and these sequences are seen frequently on a daily basis; they are easy to find once you know what to look for. Our recommendation for a simple 50ms quote expiration rule would eliminate quote-stuffing and level the playing field without impacting legitimate trading. Added 06/25/2010: It is important to note that we understand 5,000 quotes in one second on any given issue would pose no problem. However, consider that there are approx. 4,000 stocks listed on the NYSE and 9 reporting exchanges. If each reporting exchange for each stock quoted at 5,000 per second this would work out to 180,000,000 quotes per second. Furthermore 5,000 quotes per second is 5 changes per millisecond. At those rates you'd have to abandon the concept of market orders entirely. In fact, at rates exceeding even 50 quotes per second/stock you'd have to abandon market orders entirely. Some would also point out that you couldn't change the prices at those rates due to the bid/ask spread being so narrow. However there are plenty of cases where the price remains fixed and the sizes flutter. Furthermore, a CQS quote is 58 or 102 bytes depending if it's a short or long quote respectively. If the bbo is affected, then add 28 or 58 bytes for a short or long appendage respectively (if the goal is to stuff everyone, you can be sure it would require a long quote and affect the bbo). This equates to a minimum size of (5,000 x 58) 290,000 bytes per second and a maximum size of ((102+58) x 5,000) 800,000 bytes per second for 1 exchange for 1 stock. As a T1 line is 150,000 bytes/sec, one stock ticking away at the minimum 290,000 bytes per second would jam two T1 lines. |

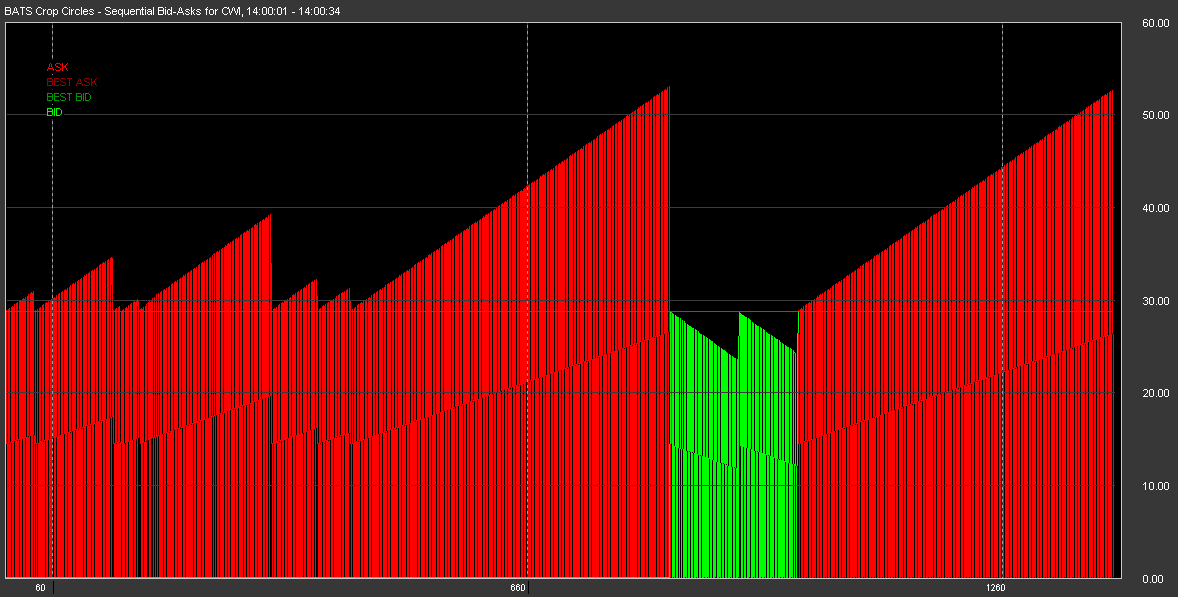

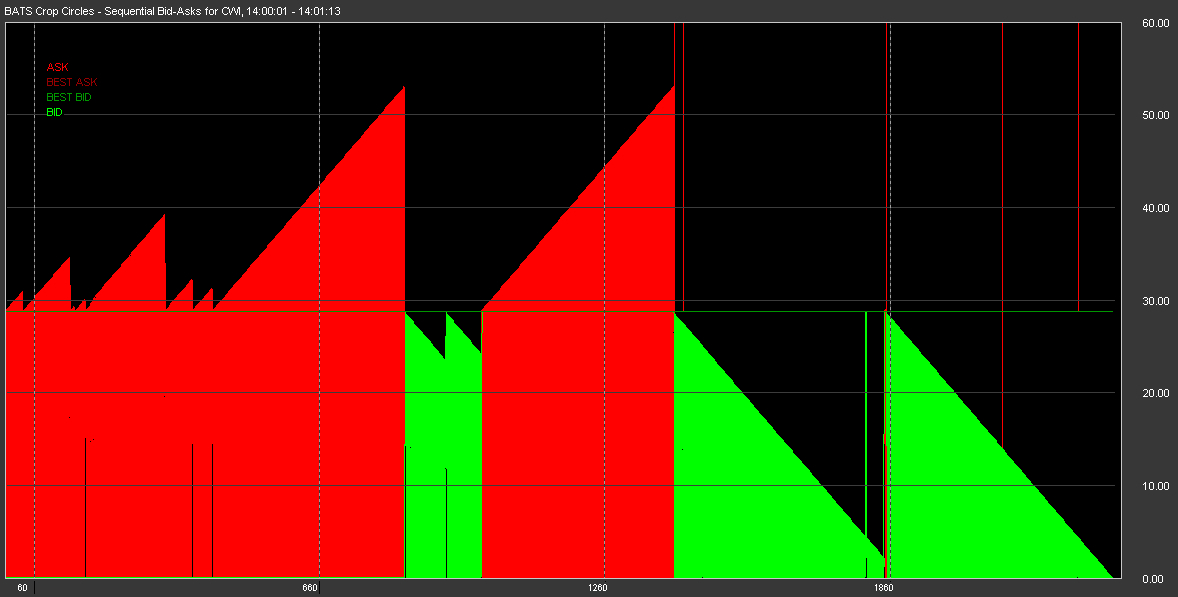

| The BATS exchange generates data that is SO unusual and bizarre that we now

refer to them as the "Crop Circle" formations and have given the

formations unique names. If one did not know better they would almost be

inclined to consider this some type of virus in the BATS software. While in not

all cases, the majority of the sequence quotes are staggered between valid

quotes and stub quotes. Volume of these erroneous quotes can be enormous on any

given burst or sequence and can last anywhere from a few hundred milliseconds

to a few entire seconds. |

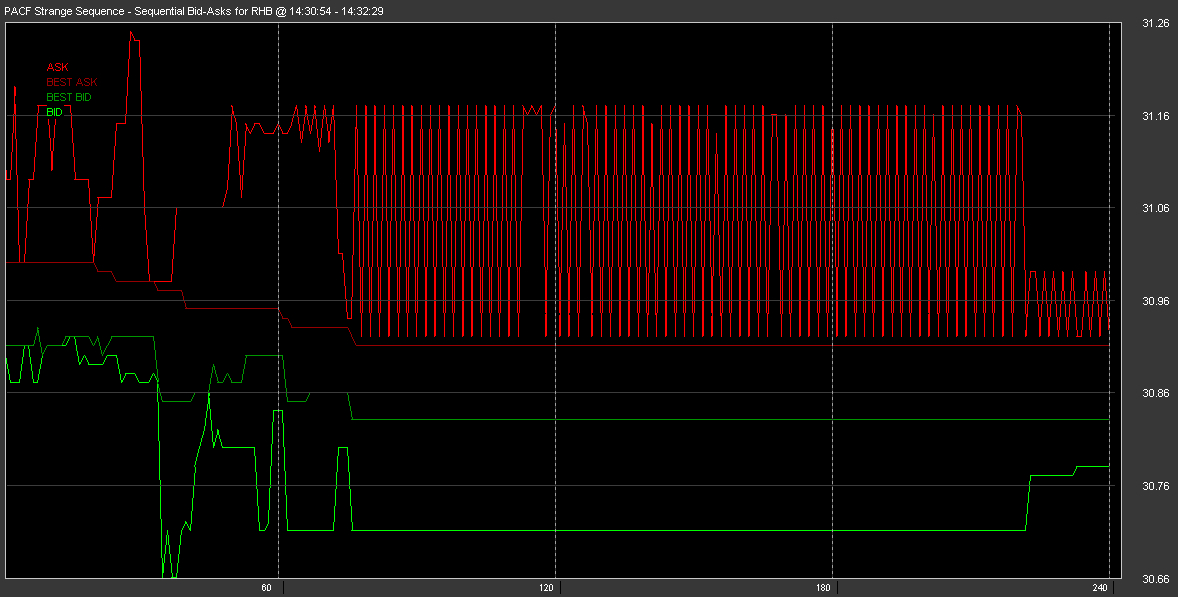

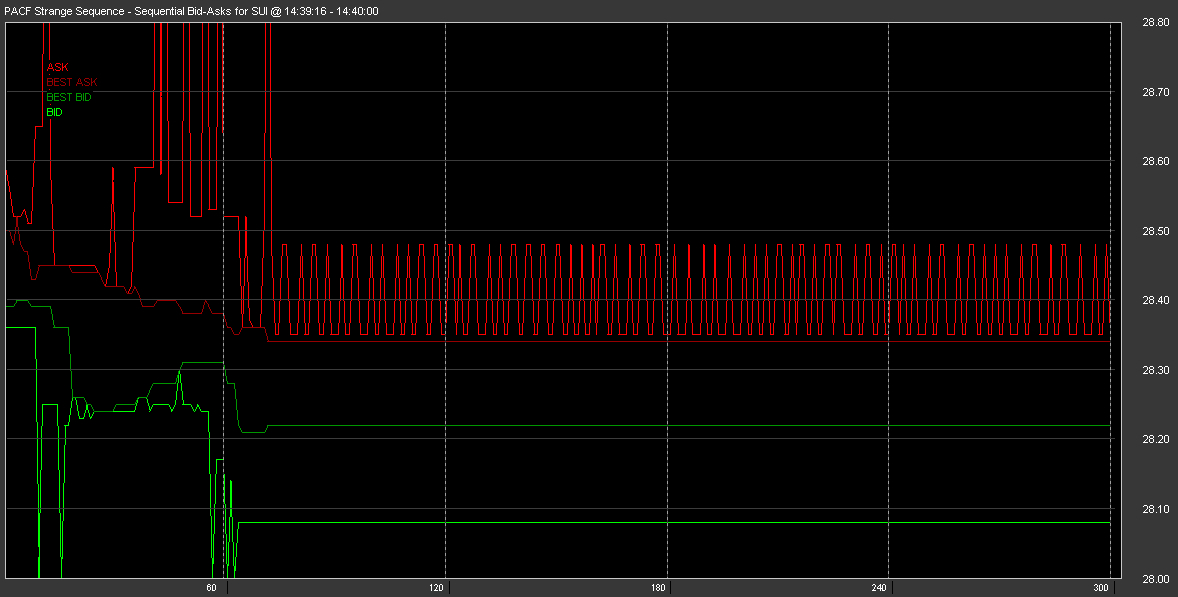

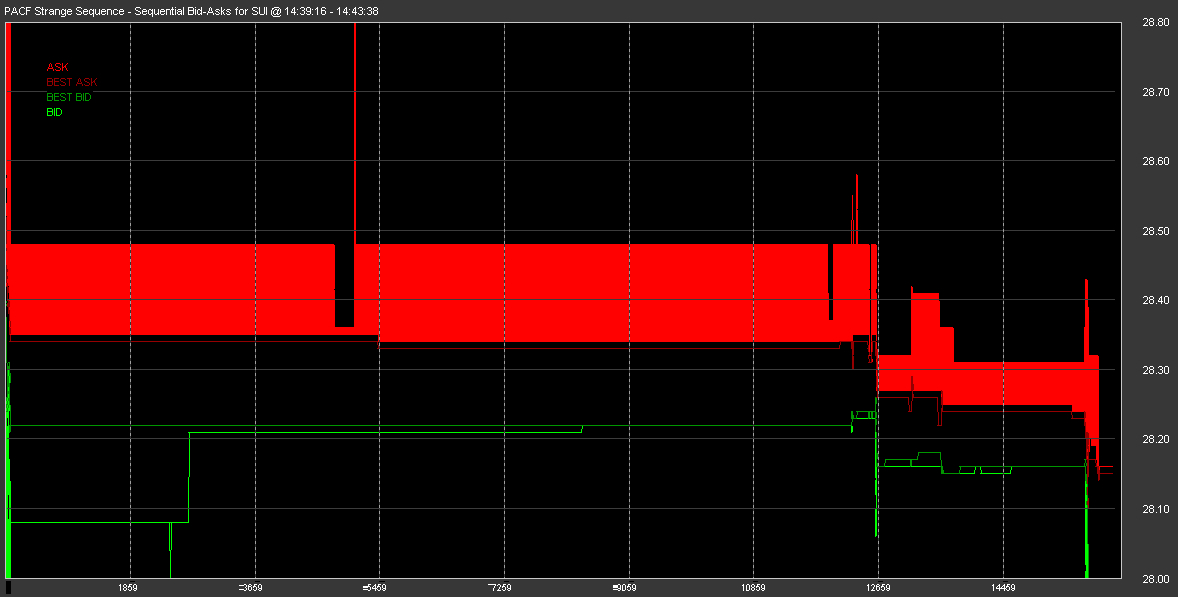

| While less extreme than the BATS sequences, PACF also generates fluttering

sequences of quote prices. Generally speaking these prices stay near the BBO

prices. Like BATS, the PACF sequences can last anywhere from a few hundred

milliseconds to a few entire seconds. |

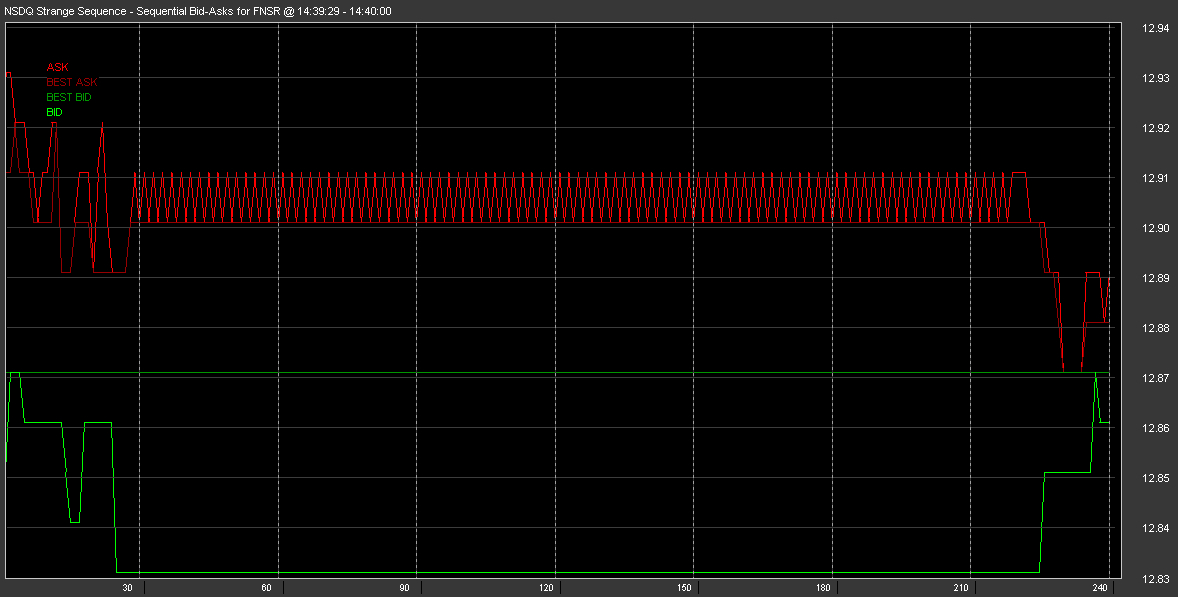

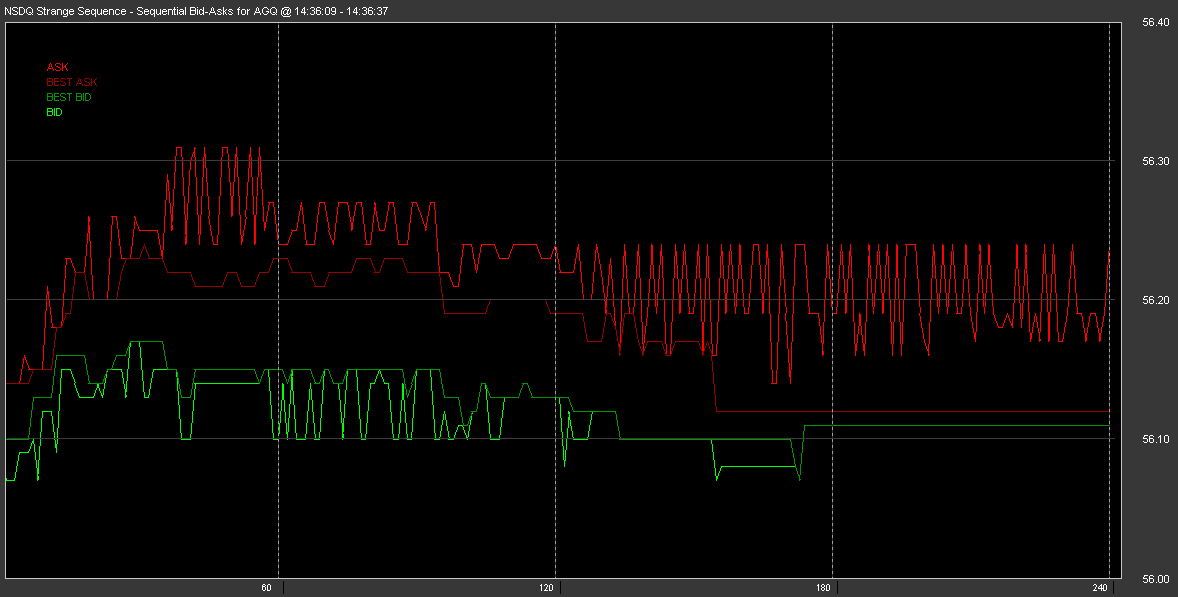

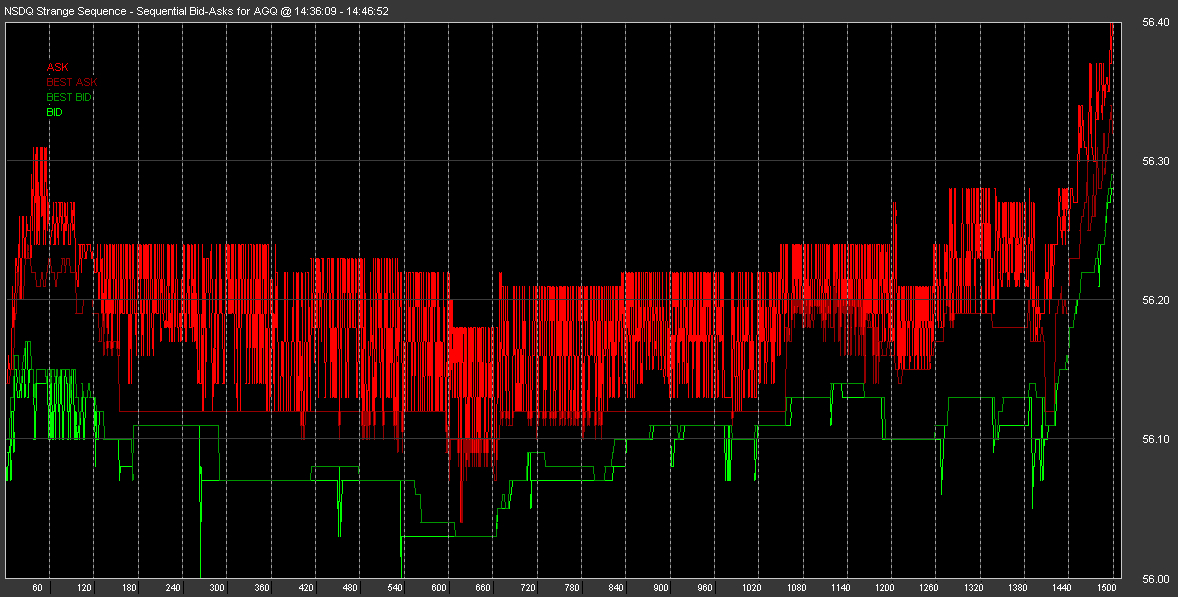

| Like PACF, the NSDQ sequences are less extreme than the BATS sequences but

will generate fluttering sequences of quote prices. Generally speaking these

prices stay near the BBO prices however in many cases they can be quite a

distance from the BBO. Like BATS and PACF, the NSDQ sequences can last anywhere

from a few hundred milliseconds to a few entire seconds. |

| Supporting Data: 0506_MPW.txt 0506_RHB.txt 0506_SUI.txt 0506_FNSR.txt 0506_AGQ.txt |

| This report and all material shown on this website is published by Nanex, LLC and may not be reproduced, disseminated, or distributed, in part or in whole, by any means, outside of the recipient's organization without express written authorization from Nanex. It is a violation of federal copyright law to reproduce all or part of this publication or its contents by any means. This material does not constitute a solicitation for the purchase or sale of any securities or investments. The opinions expressed herein are based on publicly available information and are considered reliable. However, Nanex makes NO WARRANTIES OR REPRESENTATIONS OF ANY SORT with respect to this report. Any person using this material does so solely at their own risk and Nanex and/or its employees shall be under no liability whatsoever in any respect thereof. |